What Is An FHA Loan?

An FHA loan is a type of mortgage insured by the Federal Housing Administration (FHA), a government agency that aims to make homeownership more accessible, particularly for first-time buyers and individuals with lower credit scores or smaller down payments. Here’s a breakdown of what an FHA loan is and how it works:

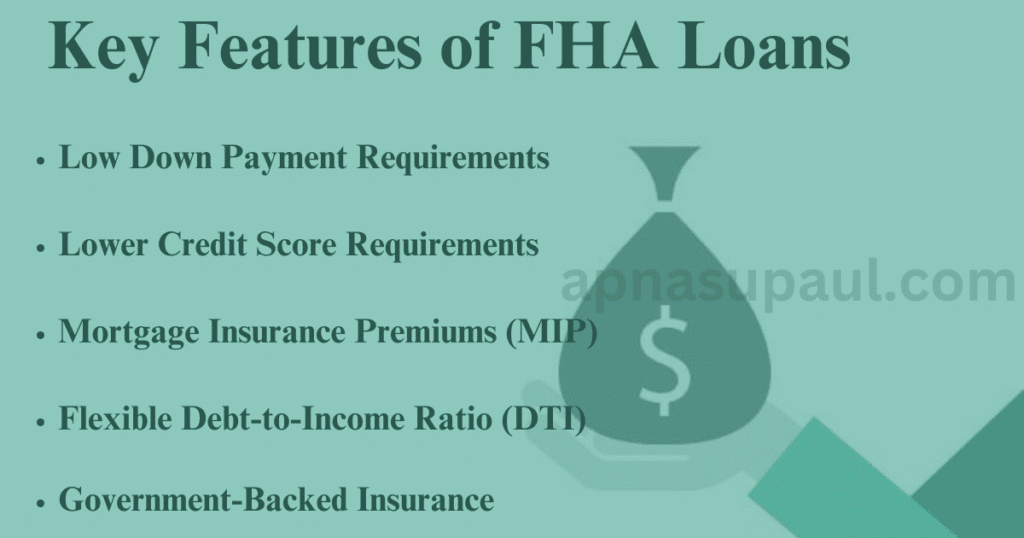

Key Features of FHA Loans

Low Down Payment Requirements

- Borrowers can qualify with as little as 3.5% of the home’s purchase price for a down payment if their credit score is 580 or higher.

- For credit scores between 500 and 579, a 10% down payment is required.

Lower Credit Score Requirements

- FHA loans are more lenient on credit score requirements compared to conventional loans.

- Borrowers with scores as low as 500 can be eligible (though lenders may impose stricter requirements).

Mortgage Insurance Premiums (MIP)

- Borrowers must pay an upfront mortgage insurance premium (UFMIP) (typically 1.75% of the loan amount) and annual mortgage insurance premiums (ranging from 0.45% to 1.05% of the loan amount annually).

- These premiums protect the lender if the borrower defaults on the loan.

Flexible Debt-to-Income Ratio (DTI)

- FHA loans allow higher DTI ratios than conventional loans, making it easier for those with existing debt to qualify.

Government-Backed Insurance

- The FHA insures the loan, reducing risk for the lender and encouraging them to offer loans to a broader range of borrowers.

How FHA Loans Work

Application Process

- Borrowers apply for an FHA loan through an FHA-approved lender. The lender evaluates the borrower’s creditworthiness, income, and other factors to determine eligibility.

Loan Limits

- FHA loans have borrowing limits that vary by location and property type. These limits are based on median home prices in the area.

Property Requirements

- The home must meet FHA property standards and be used as the borrower’s primary residence.

- Inspections and appraisals must be conducted to ensure the property is safe and livable.

Approval and Closing

- Once approved, the borrower pays the required down payment and closing costs.

- The FHA ensures the loan, and the borrower begins making monthly payments, which include principal, interest, taxes, insurance, and the mortgage insurance premium.

Pros of FHA Loans & Cons of FHA Loans

Who Should Consider an FHA Loan?

- First-time homebuyers with limited savings or lower credit scores.

- Borrowers seeking to qualify with higher DTI ratios.

- Individuals purchasing homes in areas where FHA loan limits meet their needs.

FHA Loan Limits

- FHA loan limits vary based on the county and type of property (single-family home, duplex, etc.).

- Limits are tied to the area’s median home price and are adjusted annually.

- For 2024:

- Low-cost areas: $472,030 for a single-family home.

- High-cost areas: Up to $1,089,300 for a single-family home.

- For 2024:

- You can find your local FHA loan limit through the FHA’s website or by consulting a lender.

Steps to Apply for an FHA Loan

Determine Eligibility

- Check your credit score, income, and savings.

Find an FHA-Approved Lender

- Work with lenders experienced in FHA loans.

Get Pre-Approved

- Pre-approval gives you a budget and shows sellers you’re a serious buyer.

Choose a Property

- Ensure the home meets FHA standards.

Complete the Application

- Submit required documents (e.g., pay stubs, tax returns, credit report).

Close the Loan

- Pay closing costs and start making monthly payments.

Is an FHA Loan Right for You?

An FHA loan is ideal for buyers who:

- Have a lower credit score or limited savings for a down payment.

- Are purchasing in an area with FHA loan limits that meet their needs.

- Prefer a more accessible pathway to homeownership.

Also Read: How To Improve Your Credit Score For Better Loan Offers